Options Trading Fundamentals: From Theory to Iron Condor Mastery

This report offers a comprehensive guide to options trading, from foundational concepts to advanced iron condor strategies. It delves into options pricing theory, the four basic positions, and vertical spreads, culminating in a detailed exploration of the iron condor and its effectiveness in dividend ex-date scenarios.

"The market rewards patience, punishes panic, and occasionally winks at those who understand the anomaly."

— Solar Kitties Research

---

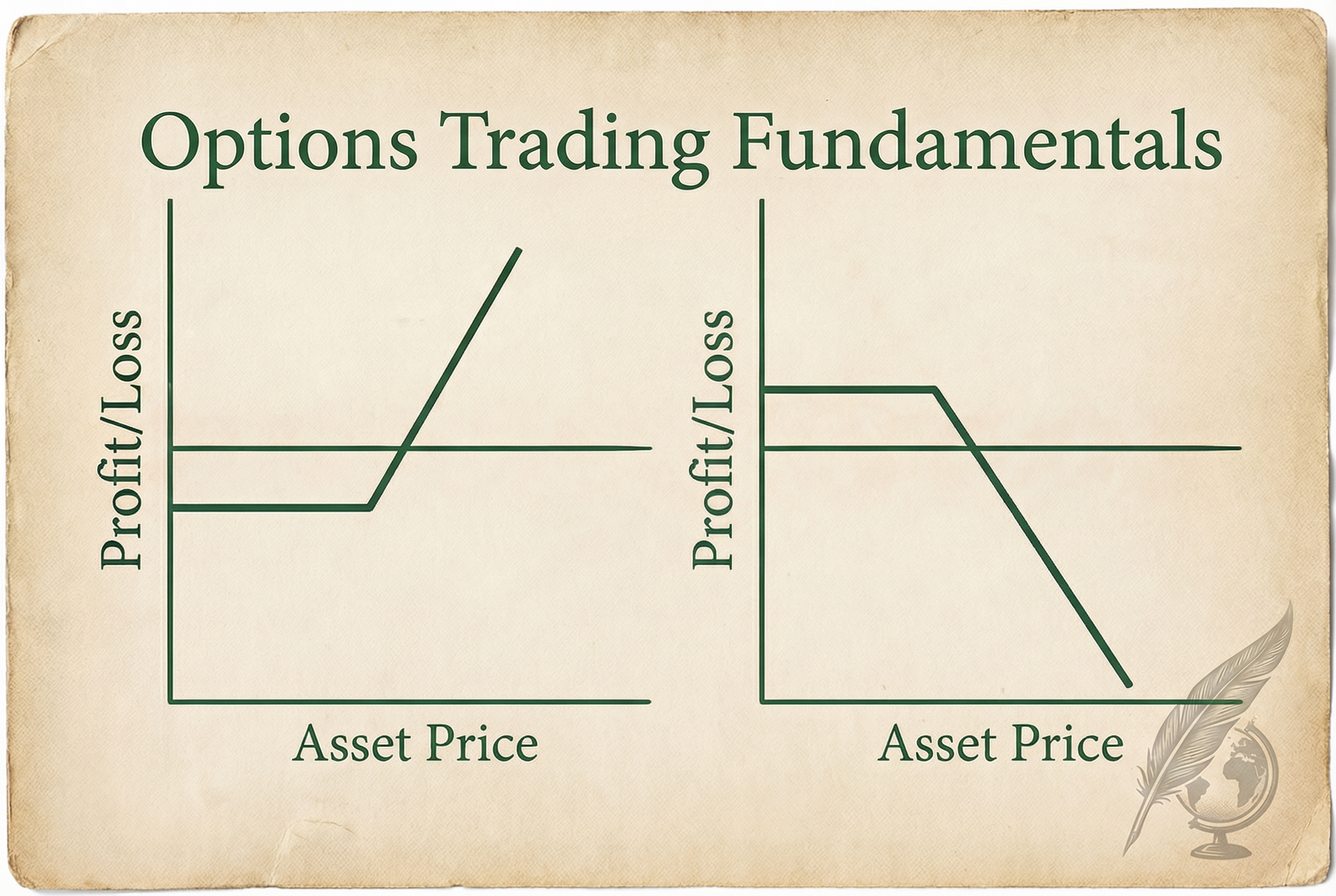

Options Payoff Diagrams: Understanding how calls and puts behave at expiration is the foundation for constructing iron condors and other defined-risk strategies.

This report provides a comprehensive guide to understanding and trading options, starting from the foundational theories of option pricing and moving to the practical application of advanced strategies like the iron condor.

We will explore how these strategies can be effectively employed, particularly in the context of dividend ex-date scenarios, a specialized area where the Dividend Anomaly platform has demonstrated a historical 92.3% win rate over 78 backtested trades.

The success of the Dividend Anomaly platform is a testament to the power of a systematic, data-driven approach to trading, and this report will provide you with the foundational knowledge to understand and potentially replicate this success.

An option is a contract that grants the buyer the right, but not the obligation, to buy or sell an underlying financial asset at a predetermined price, known as the strike price, on or before a specific date, known as the expiration date.

As derivatives, options derive their value from an underlying asset, such as a stock, index, or commodity. For buyers, options provide the potential for significant leverage and strictly defined risk. For sellers, they offer a means of generating income through the collection of option premiums.

The two fundamental types of options are calls and puts, which form the building blocks for a vast array of trading strategies.

A call option gives the holder the right to buy an underlying asset at the strike price. Investors buy calls when they are bullish, anticipating that the asset's price will rise significantly.

Conversely, a put option gives the holder the right to sell an underlying asset at the strike price. Investors buy puts when they are bearish, expecting the asset's price to decline.

Options Pricing Theory

To trade options effectively, one must first grasp the principles that govern their valuation. The theoretical value of an option is influenced by several factors, including the underlying asset's price, the strike price, the time to expiration, the risk-free interest rate, and the volatility of the underlying asset.

Two cornerstone concepts in options pricing are the Black-Scholes Model and the principle of Put-Call Parity.

The Black-Scholes Model

The Black-Scholes model, developed by Fischer Black and Myron Scholes in 1973, is a Nobel Prize-winning mathematical model for pricing European-style options.

It provides a theoretical estimate of an option's price based on the factors mentioned above. The model's formulas for call (C) and put (P) options are as follows [1]:

C(S, t) = N(d1)S - N(d2)Ke^(-r(T-t))

P(S, t) = N(-d2)Ke^(-r(T-t)) - N(-d1)S

While the formulas themselves are complex, the model's real value for most traders lies in its output: the "Greeks."

The Greeks are a set of risk measures that describe the sensitivity of an option's price to changes in the various factors that affect it.

| Measures Sensitivity To | Impact on Long Call |

|---|---|

| Underlying Asset Price | Positive |

| Delta | Positive |

| Time Decay | Negative |

| Implied Volatility | Positive |

| Interest Rates | Positive |

- Delta measures the rate of change of an option's price with respect to a $1 change in the underlying asset's price. For example, a call option with a delta of 0.50 is expected to increase in value by $0.50 for every $1 increase in the underlying stock's price. Delta is not a static number; it changes as the stock price changes. As a call option gets deeper in the money, its delta approaches 1.0. As it gets further out of the money, its delta approaches 0.

- Gamma measures the rate of change in an option's delta with respect to a $1 change in the underlying asset's price. It represents the convexity of the option's value. Gamma is highest for at-the-money options and decreases as the option moves further in- or out-of-the-money. High gamma means that the delta will change rapidly with changes in the underlying price, which can be a double-edged sword.

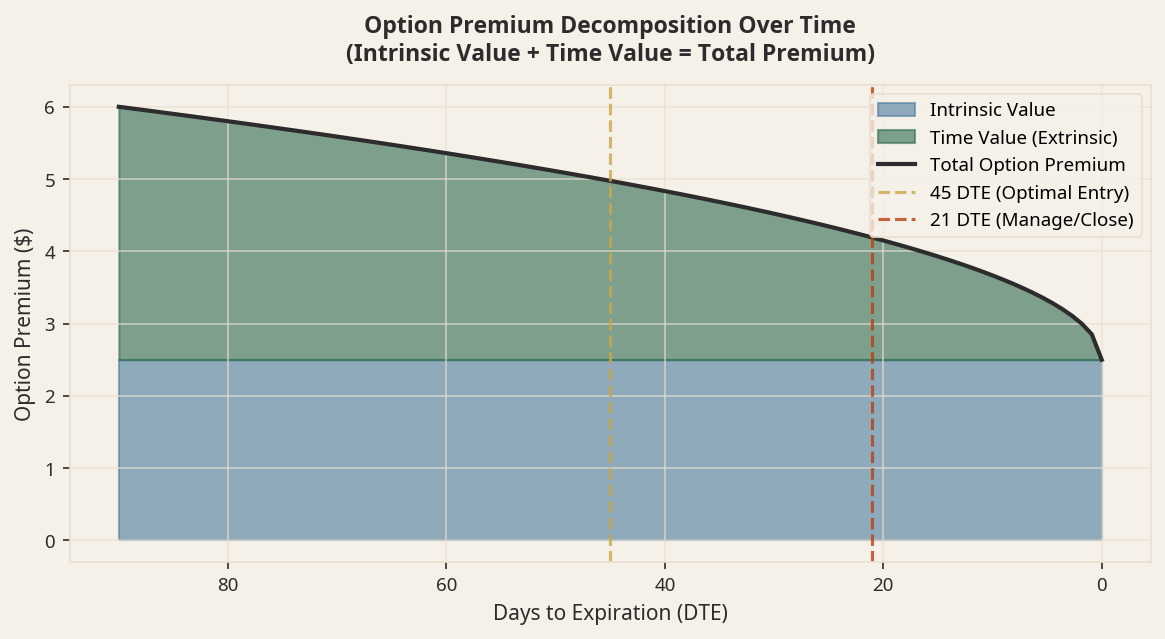

- Theta measures the rate of decline in an option's value due to the passage of time. It is often referred to as "time decay." Theta is generally negative for long options, as the passage of time erodes the value of the option. The rate of theta decay accelerates as an option approaches its expiration date.

- Vega measures the rate of change in an option's value with respect to a 1% change in the implied volatility of the underlying asset. Vega is highest for at-the-money options with longer times to expiration. Long options have positive vega, meaning they increase in value as implied volatility rises. Short options have negative vega, meaning they profit from a decrease in implied volatility.

- Rho measures the sensitivity of an option's price to changes in the risk-free interest rate. Rho is generally not a significant factor for most retail options traders, as interest rate changes are typically small and have a minimal impact on option prices, especially for shorter-dated options.

Put-Call Parity

Put-call parity is a fundamental principle in options pricing that describes the relationship between the price of a European call option and a European put option with the same underlying asset, strike price, and expiration date.

The relationship is expressed by the following formula [2]:

C + PV(K) = P + S

Where:

- C = Price of the call option

- PV(K) = Present value of the strike price (K), discounted at the risk-free rate

- P = Price of the put option

- S = Price of the underlying asset

This principle dictates that the price of a call option implies the price of a corresponding put option, and vice versa. If this relationship does not hold, a risk-free arbitrage opportunity exists.

For example, if the call price is too low relative to the put price, an arbitrageur could buy the call, sell the put, and sell the underlying stock to lock in a risk-free profit. This arbitrage activity ensures that put-call parity generally holds in the market.

The Four Basic Options Positions

Every options trading strategy, no matter how complex, is built upon four basic positions:

- Long Call: The purchase of a call option. This is a bullish strategy with limited risk (the premium paid) and unlimited profit potential. The position profits as the underlying asset's price rises above the strike price.

- Short Call: The sale of a call option. This is a bearish or neutral strategy with limited profit potential (the premium received) and unlimited risk. The position profits if the underlying asset's price remains below the strike price.

- Long Put: The purchase of a put option. This is a bearish strategy with limited risk (the premium paid) and substantial profit potential. The position profits as the underlying asset's price falls below the strike price.

- Short Put: The sale of a put option. This is a bullish or neutral strategy with limited profit potential (the premium received) and substantial risk. The position profits if the underlying asset's price remains above the strike price.

Building on the Basics: Vertical Spreads

A vertical spread is an options strategy that involves the simultaneous purchase and sale of options of the same type (either calls or puts) and with the same expiration date, but with different strike prices.

Spreads are used to define risk and create a specific risk/reward profile.

| Strategy | Market Outlook | Max Profit |

|---|---|---|

| Buy lower strike call, sell higher strike call | Moderately Bullish | Difference in strikes - Net Debit |

| Sell lower strike call, buy higher strike call | Moderately Bearish | Net Credit Received |

| Sell higher strike put, buy lower strike put | Moderately Bullish | Net Credit Received |

| Buy higher strike put, sell lower strike put | Moderately Bearish | Difference in strikes - Net Debit |

Bull Call Spread

A bull call spread is a bullish strategy that involves buying a call option and simultaneously selling another call option with a higher strike price.

This strategy limits both the potential profit and the potential loss of the trade. The maximum profit is the difference between the two strike prices, less the net debit paid to enter the position. The maximum loss is the net debit paid.

For example, if a trader buys a $50 strike call for $2 and sells a $55 strike call for $1, the net debit is $1. The maximum profit is $4 ($5 - $1), and the maximum loss is $1.

Bear Put Spread

A bear put spread is a bearish strategy that involves buying a put option and simultaneously selling another put option with a lower strike price.

This strategy also limits both the potential profit and the potential loss. The maximum profit is the difference between the two strike prices, less the net debit paid. The maximum loss is the net debit paid.

For example, if a trader buys a $50 strike put for $2 and sells a $45 strike put for $1, the net debit is $1. The maximum profit is $4 ($5 - $1), and the maximum loss is $1.

Mastering the Iron Condor

The iron condor is an advanced, non-directional options strategy that is designed to profit from a stock that is expected to trade within a specific price range.

It is a combination of two vertical spreads: a bull put spread and a bear call spread.

What is an Iron Condor?

An iron condor is constructed by selling an out-of-the-money put spread and an out-of-the-money call spread with the same expiration date.

The strategy involves four separate option legs:

- Buy one out-of-the-money put option (long put).

- Sell one out-of-the-money put option with a higher strike price (short put).

- Sell one out-of-the-money call option (short call).

- Buy one out-of-the-money call option with a higher strike price (long call).

The goal is for the underlying asset's price to remain between the two short strike prices at expiration. If this occurs, all four options expire worthless, and the trader keeps the net premium received when opening the position.

P/L Diagram Explained

The profit/loss (P/L) diagram of an iron condor has a distinctive shape, resembling the wings of a condor.

The maximum profit is the net credit received when initiating the trade. This is achieved if the underlying asset's price at expiration is between the strike prices of the short put and the short call.

The maximum loss is the difference between the strike prices of either the call spread or the put spread, minus the net credit received. The breakeven points are the prices at which the trade neither makes nor loses money.

There are two breakeven points: the short call strike plus the net credit, and the short put strike minus the net credit. The shape of the P/L diagram clearly illustrates the defined-risk nature of the strategy, with a flat top representing the maximum profit zone and two flat bottoms representing the maximum loss zones.

Iron Condors for Dividend Ex-Date Strategies

The iron condor strategy is particularly well-suited for trading around dividend ex-dates.

This is due to a confluence of factors that create a high-probability trading environment.

Theta Decay

Theta, or time decay, is a powerful ally for options sellers. As an option approaches its expiration date, the rate of time decay accelerates.

For an iron condor, which is a net-short premium strategy, theta decay works in the trader's favor, eroding the value of the options that were sold. This is especially true for short-term options, which have the highest rate of theta decay.

The Dividend Anomaly strategy specifically targets these short-term opportunities to maximize the impact of theta decay.

Mean Reversion

Mean reversion is the tendency of an asset's price to revert to its long-term average. In the context of dividend-paying stocks, there is often a predictable pattern of price behavior around the ex-dividend date.

The stock price tends to drop by approximately the amount of the dividend on the ex-dividend date, and then recover in the following days. This predictable, range-bound price action is ideal for an iron condor, which profits from the stock staying within a defined range.

Volatility Crush

Implied volatility (IV) is a critical component of an option's price. It represents the market's expectation of future price fluctuations.

IV tends to rise in anticipation of significant events, such as earnings announcements or dividend payments. This pre-event rise in IV is known as "IV expansion."

After the event has passed, IV typically plummets, a phenomenon known as "volatility crush." Because an iron condor is a short-volatility strategy, it profits from this post-event decline in implied volatility. The Dividend Anomaly system is designed to identify stocks with a history of significant IV crush around their dividend dates.

Practical Application

Entry Timing

The optimal time to enter an iron condor for a dividend capture strategy is typically a few days to a week before the ex-dividend date.

This allows the trader to capitalize on the elevated implied volatility before the dividend is paid. Entering too early may expose the trade to unnecessary market risk, while entering too late may result in a smaller premium due to the already-decayed time value.

Strike Selection

Proper strike selection is paramount to the success of an iron condor. The short strikes should be placed at a level where there is a low probability of the stock price reaching them.

Many traders use delta as a guide for strike selection, often choosing short strikes with a delta of around 0.10 to 0.15. This means that there is a 10-15% probability of the stock price reaching the short strike at expiration.

The width of the spread between the short and long strikes will determine the risk/reward profile of the trade. A wider spread offers a higher potential profit but also a higher potential loss. The Dividend Anomaly system uses a proprietary algorithm to identify the optimal strike prices based on historical volatility and other factors.

Exit Management

A well-defined exit plan is essential for managing risk and locking in profits. Many traders will close an iron condor for a profit when it has reached a certain percentage of its maximum potential, such as 50%.

This allows the trader to realize a profit and reduce the risk of the trade moving against them. It is also crucial to have a plan for managing losing trades.

This may involve closing the trade for a small loss or adjusting the position by "rolling" it to a different expiration date or strike price. The Dividend Anomaly system provides clear exit signals based on its backtested data.

Risk Management for Iron Condors

While the iron condor is a defined-risk strategy, it is still essential to have a robust risk management plan in place.

This includes position sizing, diversification, and having a clear understanding of the maximum potential loss on each trade. It is also important to be aware of the risk of early assignment on the short options, especially for dividend-paying stocks.

To mitigate this risk, traders should avoid holding short calls on stocks that are going ex-dividend.

Common Mistakes and How to Avoid Them

- Trading Without a Plan: The most common mistake new traders make is entering a trade without a clear plan for how they will manage it. Before entering any trade, you should know your profit target, your maximum acceptable loss, and what you will do if the trade moves against you.

- Ignoring Implied Volatility: Failing to consider the level of implied volatility is a recipe for disaster. Selling options when IV is low or buying them when IV is high is a losing proposition in the long run. The Dividend Anomaly system specifically targets high IV environments to maximize the edge from volatility crush.

- Poor Strike Selection: Choosing strikes that are too aggressive can lead to frequent losses, while choosing strikes that are too conservative can result in small profits that are not worth the risk. A data-driven approach to strike selection is essential for long-term success.

- Letting Losing Trades Run: Hope is not a strategy. It is essential to cut losses quickly and move on to the next opportunity. A disciplined approach to risk management is the hallmark of a successful trader.

- Over-leveraging: The defined-risk nature of the iron condor can tempt traders to take on too much risk. It is crucial to size positions appropriately and to avoid risking more than a small percentage of your portfolio on any single trade.

Key Takeaways

- Options are powerful and flexible financial instruments that can be used to create a wide variety of trading strategies.

- The iron condor is a non-directional, defined-risk strategy that can be used to profit from a stock that is expected to trade in a range.

- The confluence of theta decay, mean reversion, and volatility crush makes the iron condor an ideal strategy for trading around dividend ex-dates.

- A deep understanding of options pricing theory, a disciplined approach to risk management, and a well-defined trading plan are essential for long-term success in options trading.

References

[1] Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. *Journal of Political Economy*, 81(3), 637-654.

[2] Stoll, H. R. (1969). The Relationship Between Put and Call Option Prices. *The Journal of Finance*, 24(5), 801-824.