A Comprehensive Framework for Growth Investing in Modern Markets

This report presents a five-pillar framework for identifying sustainable growth opportunities, drawing on research showing a small percentage of stocks drive most wealth creation. It details how to evaluate companies based on Total Addressable Market, competitive moats, unit economics, management quality, and valuation, using examples like Amazon, NVIDIA, and Tesla.

"The market rewards patience, punishes panic, and occasionally winks at those who understand the anomaly."

— Solar Kitties Research

---

Growth vs Value vs Index: A disciplined growth investing framework has historically outperformed both value strategies and passive index investing over 10-year periods.

An inconvenient truth lies at the heart of public equity markets: most stocks are duds. Over their lifetimes, the majority of publicly traded companies fail to even outperform risk-free Treasury bills.

This is not a cynical opinion, but a statistical reality laid bare by groundbreaking research. The vast majority of the stock market's incredible long-term wealth creation is not driven by the average stock, but by a tiny fraction of exceptional outlier companies.

For investors, this power-law distribution of returns changes everything. It means that the key to building transformative wealth is not just picking good companies, but identifying and holding these rare, hyper-performing businesses.

This report presents a comprehensive framework for just that. We will move beyond simplistic metrics and delve into a systematic, five-pillar evaluation process designed to help investors identify the next generation of sustainable growth opportunities.

By understanding the forces that create market-defining companies, investors can increase their odds of capturing the extraordinary returns that a select few businesses generate. We will explore this framework through the lens of modern titans like Amazon, NVIDIA, and Tesla, dissecting their DNA to understand what makes them exceptional. This is a blueprint for growth investing in modern markets.

The Power Law of Market Returns: Why Outliers Are Everything

The conventional wisdom of diversification, while sound for mitigating risk, often obscures a more fundamental truth about where returns actually come from. The idea that a rising tide lifts all boats is a dangerous simplification in the stock market.

A landmark 2018 study by Professor Hendrik Bessembinder, "Do stocks outperform Treasury bills?", rigorously quantified this phenomenon, and the findings are staggering. [1]

Analyzing the performance of every U.S. common stock from 1926 to 2016, Bessembinder found that the entire net gain in the U.S. stock market—nearly $35 trillion in wealth creation—was generated by the top-performing 4% of companies.

The other 96% of stocks, as a group, collectively only managed to match the return of risk-free one-month Treasury bills. More than half of all stocks that have ever been listed delivered negative lifetime returns.

The single most frequent outcome (when returns are rounded to the nearest 5%) observed for individual common stocks over their full lifetimes is a loss of 100%.

This research reveals that the stock market is not a game of averages; it is a game of outliers. The spectacular success of a few big winners compensates for the mediocre or value-destroying performance of the vast majority.

This has profound implications for investors. It suggests that the traditional approach of seeking modest outperformance with a broadly diversified portfolio of 'good enough' companies is a suboptimal strategy for long-term wealth creation.

To truly move the needle, an investor's primary focus must be on identifying and owning the small handful of companies with the potential to become the next market leaders.

This is the philosophical underpinning of growth investing. It is an explicit search for the 4%—the companies with the vision, the market opportunity, and the competitive resilience to generate returns that are not just better than average, but orders of magnitude greater. The following framework is a systematic process for conducting that search.

A Five-Pillar Framework for Identifying Growth Opportunities

To systematically identify companies with the potential to become part of the top 4%, we need a structured approach that goes beyond surface-level metrics.

This five-pillar framework provides a robust model for evaluating potential growth investments. Each pillar represents a critical hurdle a company must clear to be considered a candidate for long-term, outlier returns.

Pillar 1: Total Addressable Market (TAM)

The starting point for any growth investment thesis must be the size and growth of the company's market. The Total Addressable Market (TAM) represents the total revenue opportunity available for a product or service if a company were to achieve 100% market share.

A company simply cannot become a multi-billion dollar giant if it is operating in a niche, multi-million dollar market. A vast and expanding TAM is the fuel for hyper-growth.

Investors should look for companies operating in markets that are not only large today but are also projected to grow significantly in the future. This can be driven by secular trends, technological shifts, or new business models that unlock previously untapped demand.

There are three primary methods for estimating TAM:

- Top-Down Analysis: This method starts with a large, overall market size and narrows it down based on relevant segments. For example, to estimate the TAM for a new electric vehicle, one might start with the total global automotive market and then filter down to the relevant vehicle class and geographic regions.

- Bottom-Up Analysis: This is a more granular approach that involves identifying the total number of potential customers and multiplying that by the average revenue per customer. For a SaaS company, this would involve estimating the number of businesses that could use the software and multiplying it by the annual subscription price.

- Value Theory Analysis: This approach focuses on the value a product or service creates for its customers. By estimating this value, one can then make an educated guess as to how much customers would be willing to pay and how many customers would be interested at that price point.

Case Studies in TAM:

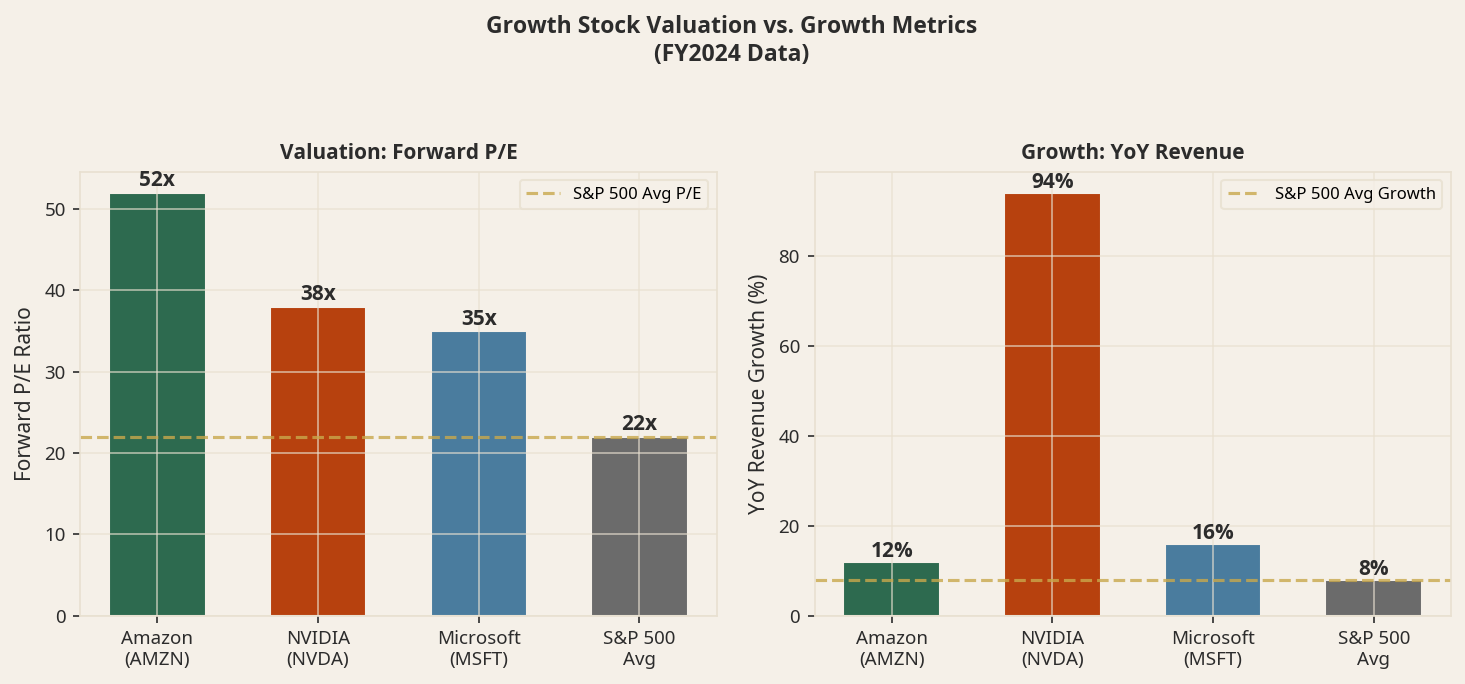

- Amazon: Amazon's genius lies in its continuous expansion of its TAM. It started with books, then expanded to all of e-commerce. With Amazon Web Services (AWS), it entered the enormous market of enterprise IT infrastructure. Now, with ventures into advertising, healthcare, and logistics, its TAM is a multi-trillion dollar opportunity.

- NVIDIA: Initially a provider of graphics cards for PC gaming, NVIDIA has masterfully expanded its TAM to include data centers, professional visualization, and, most significantly, the hardware backbone for the artificial intelligence revolution. Its TAM is no longer just about gaming; it's about the future of computing.

- Tesla: Tesla's stated mission is to accelerate the world's transition to sustainable energy. Its TAM is not just the automotive market, but the entire energy ecosystem, including energy generation (Solar Roof) and storage (Powerwall). This expansive vision is what fuels its ambitious valuation.

Pillar 2: Competitive Moat

A large TAM attracts competition. A company's ability to defend its market share and profitability over the long term depends on its competitive moat—a term popularized by Warren Buffett to describe a sustainable competitive advantage.

A strong moat protects a company from rivals, much like a real moat protects a castle. For growth investors, a widening moat is a sign of a truly exceptional business.

There are several primary sources of competitive moats, each creating a different type of barrier to entry for potential rivals. Understanding these is key to identifying durable businesses.

| Description |

|---|

| The value of a product or service increases for each new user. |

| Patents, brands, regulatory licenses, and other hard-to-copy assets. |

| The ability to produce and deliver products or services at a lower cost than competitors. |

| The expense or inconvenience a customer incurs when switching to a competitor. |

| A business model that incumbents cannot adopt without damaging their core business. |

"The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage." - Warren Buffett

Assessing the strength of a moat is a qualitative exercise, but it is crucial. Investors should ask: What prevents a well-funded competitor from stealing this company's customers?

Is that advantage getting stronger or weaker over time? A company with a strong and widening moat is well-positioned to compound its value for many years.

Pillar 3: Unit Economics

Rapid revenue growth is exciting, but it can also be a mirage. If a company is losing money on every new customer it acquires, then growth is simply accelerating the company's demise.

This is where unit economics come in. Unit economics are the direct revenues and costs associated with a particular business model on a per-unit basis. The "unit" can be a customer, a product, or a transaction.

For growth investors, two of the most important unit economic metrics are:

- Customer Lifetime Value (LTV): The total profit a business can expect to generate from a single customer over the entire duration of their relationship.

- Customer Acquisition Cost (CAC): The total cost of sales and marketing required to acquire a new customer.

The relationship between these two metrics is critical. A healthy business model requires that the LTV is significantly greater than the CAC. A common rule of thumb for SaaS companies is that the LTV/CAC ratio should be at least 3:1.

A ratio below this may indicate that the company is paying too much for growth, and the business model may not be sustainable.

Strong unit economics are a sign of a healthy, scalable business. It demonstrates that the company has found a profitable way to acquire and serve customers, and that growth is creating, not destroying, value.

For companies that are not yet profitable on a GAAP basis, a clear path to positive unit economics is an essential prerequisite for investment.

Pillar 4: Management Quality

Companies are not self-driving entities; they are led by people. The quality of a company's management team is one of the most critical—and often most overlooked—factors in its long-term success.

A visionary leader can steer a company to greatness, while a mediocre one can drive even a business with a strong moat into the ground. For growth investors, evaluating management is not just about looking at resumes; it's about assessing their vision, execution, and stewardship of shareholder capital.

Key areas to assess when evaluating management quality include:

- Vision and Strategy: Does the leadership team have a clear, compelling, and ambitious vision for the future of the company? Are they able to articulate a coherent strategy for achieving that vision? Visionary leaders like Elon Musk at Tesla and Jensen Huang at NVIDIA have been instrumental in defining and dominating new industries.

- Track Record of Execution: Ideas are cheap; execution is everything. Investors should look for a management team with a proven ability to deliver on its promises. This includes meeting product deadlines, hitting financial targets, and effectively navigating challenges.

- Capital Allocation: A CEO's primary job is to be a disciplined allocator of capital. This means making smart decisions about how to invest the company's profits—whether to reinvest in the business, acquire other companies, or return capital to shareholders. A history of value-destructive acquisitions or wasteful spending is a major red flag.

- Shareholder Alignment: Is the management team aligned with the interests of long-term shareholders? This can be assessed by looking at executive compensation structures (are they tied to long-term performance?) and insider ownership (do executives have significant skin in the game?).

Evaluating management is more of an art than a science, but it is an essential component of the investment process. Great companies are almost always led by great leaders.

Pillar 5: Valuation Discipline

The final pillar of our framework is valuation discipline. This may seem counterintuitive for a growth investing strategy, where companies often trade at high multiples of earnings or sales.

However, valuation discipline is not about buying cheap stocks; it's about not overpaying for growth. The price you pay for an asset is the ultimate anchor of your return. Paying too high a price, even for a fantastic company, can lead to years of subpar returns.

Valuing high-growth companies is notoriously difficult. Traditional metrics like the Price-to-Earnings (P/E) ratio can be misleading, as many growth companies are reinvesting so heavily in their business that they have little to no current earnings.

Instead, growth investors often use a combination of alternative metrics and qualitative judgment:

- Price-to-Sales (P/S) Ratio: This can be a useful metric for companies that are not yet profitable. It provides a sense of how much the market is willing to pay for each dollar of revenue.

- PEG Ratio: The PEG ratio compares the P/E ratio to the company's expected earnings growth rate. A PEG ratio of 1 suggests that the company is fairly valued relative to its growth prospects.

- Discounted Cash Flow (DCF) Analysis: While challenging for growth companies due to the uncertainty of future cash flows, a DCF analysis can be a valuable exercise. It forces the investor to make explicit assumptions about a company's long-term growth rate, margins, and profitability, providing a framework for assessing whether the current stock price is reasonable.

The goal of valuation discipline is not to find a precise intrinsic value, but to establish a margin of safety. It's about understanding the growth assumptions that are baked into the current stock price and assessing whether those assumptions are realistic.

If a stock's valuation implies a level of growth that is heroic or unprecedented, it may be a sign of excessive optimism and a signal to be cautious.

Scoring the Titans: A Five-Pillar Assessment

To bring the framework to life, let's apply it to our three case-study companies: Amazon, NVIDIA, and Tesla.

The table below provides a qualitative score (out of 10) for each company across the five pillars. This is not a precise science, but a structured way to compare their relative strengths.

| Amazon (AMZN) | NVIDIA (NVDA) | Tesla (TSLA) |

|---|---|---|

| 10 | 10 | 10 |

| 9 | 8 | 7 |

| 8 | 9 | 6 |

| 8 | 9 | 8 |

| 7 | 6 | 5 |

| 42/50 | 42/50 | 36/50 |

This table is a snapshot in time and the scores will evolve. However, it demonstrates how the framework can be used to create a disciplined, comparative analysis of growth opportunities.

The Unique Risks of Growth Investing

While the potential rewards are substantial, growth investing comes with its own unique set of risks that investors must be prepared to manage.

- Multiple Compression: High-growth stocks often trade at high valuation multiples. If a company's growth rate slows, even slightly, the market may re-rate the stock at a much lower multiple, leading to a sharp decline in the stock price even if the business itself remains healthy.

- Narrative Shifts: Growth stocks are often fueled by a powerful narrative about the future. If that narrative is challenged—by a new competitor, a technological shift, or a change in consumer preferences—the stock can fall dramatically. The story is often as important as the numbers.

- Execution Risk: Young, high-growth companies are often attempting to do things that have never been done before. There is a significant risk that they will fail to execute on their ambitious plans, leading to disappointment and a loss of investor confidence.

Integrating Growth and Income

For many investors, a pure growth strategy may be too volatile. A powerful approach is to combine a portfolio of high-conviction growth stocks with a foundation of high-quality, dividend-paying companies.

This creates a more balanced portfolio that can generate both capital appreciation and a steady stream of income.

The Dividend Anomaly platform, with its focus on generating consistent income through options strategies on dividend-paying stocks, can be an excellent complement to a growth-oriented portfolio. The income generated from these strategies can be used to:

- Reinvest in growth positions: Use the cash flow from dividend strategies to add to your best growth ideas, especially during market downturns.

- Reduce portfolio volatility: The steady income can help to cushion the portfolio during periods of market stress when growth stocks may be underperforming.

- Provide a source of liquidity: The income can provide a source of cash for living expenses without the need to sell long-term growth holdings.

By combining the search for outlier returns with a disciplined income-generation strategy, investors can build a robust, all-weather portfolio.

Key Takeaways

- The stock market follows a power-law distribution, where a small number of outlier companies drive the vast majority of wealth creation.

- To identify these outliers, investors need a disciplined framework that goes beyond traditional valuation metrics.

- The five-pillar framework—Total Addressable Market, Competitive Moat, Unit Economics, Management Quality, and Valuation Discipline—provides a robust model for evaluating growth opportunities.

- Growth investing carries unique risks, including multiple compression and narrative shifts, which must be carefully managed.

- Combining a growth strategy with a dividend-based income strategy can create a balanced and resilient portfolio.

References

[1] Bessembinder, H. (2018). Do stocks outperform Treasury bills? Journal of Financial Economics, 129(3), 440-457. https://doi.org/10.1016/j.jfineco.2018.06.004