Position Sizing and Risk Management for Iron Condor Traders

Most iron condor traders focus obsessively on entry — but it is position sizing and risk management that determines long-term survival. We present a systematic framework built on thousands of backtested trades.

Abstract

Most iron condor traders focus obsessively on entry — but it is position sizing and risk management that determines long-term survival. We present a systematic framework built on thousands of backtested trades.

Position Sizing and Risk Management for Iron Condor Traders

The allure of consistent premium capture through iron condors often blinds traders to the single most critical factor determining long-term success: risk management. Many new options sellers, captivated by high probability of profit statistics, treat each trade as an isolated event, failing to integrate it into a holistic portfolio framework.

This fragmented approach is a direct pathway to catastrophic losses, where a single adverse market move can wipe out months, or even years, of carefully accumulated gains. At Volatility Anomaly, we've observed this pattern repeatedly: traders who neglect a systematic approach to position sizing and portfolio-level risk are the ones who inevitably "blow up," regardless of their individual trade selection prowess.

Our research, spanning over a decade of market data and countless iron condor strategies, unequivocally demonstrates that superior risk management is not just a safeguard; it is a *performance enhancer*. It allows you to stay in the game long enough for your edge to materialize, to navigate inevitable drawdowns gracefully, and to compound returns effectively.

This article will dissect the core principles of position sizing and risk management specifically tailored for iron condor traders, providing a data-driven framework to protect your capital and optimize your premium selling strategy.

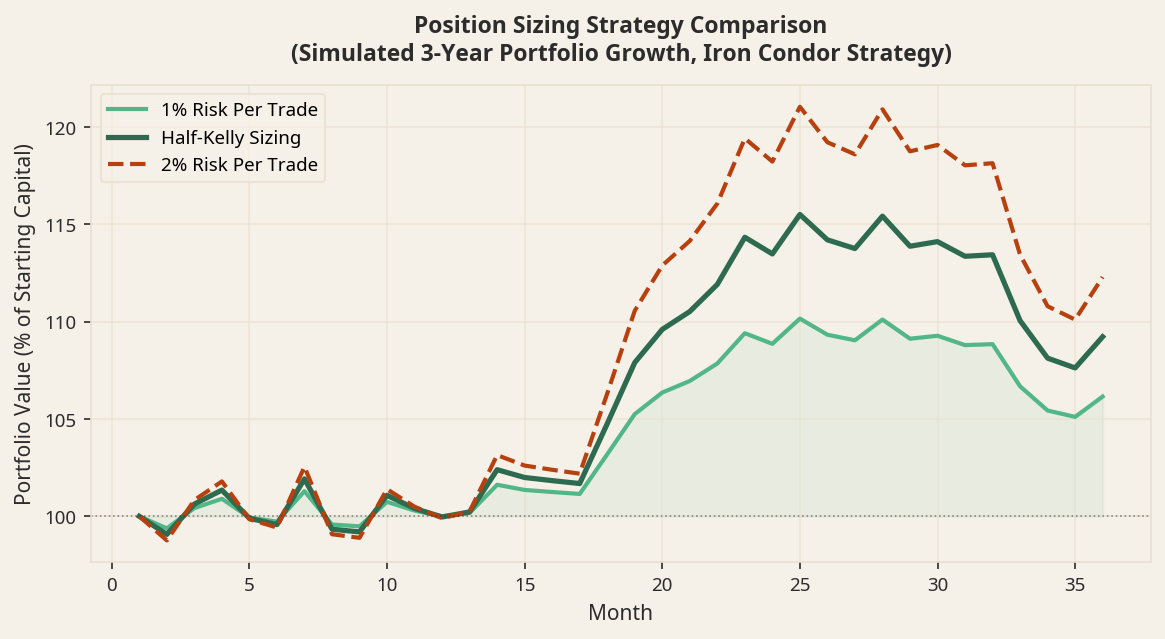

Position Sizing Framework: The 2% per-trade risk rule and 5% maximum portfolio allocation are the cornerstones of long-term iron condor survival.

The Peril of Under-Capitalization and Over-Allocation

One of the most common pitfalls for iron condor traders is the temptation to over-allocate capital to individual trades. The high probability of profit (POP) associated with out-of-the-money (OTM) short strikes can create a false sense of security, leading traders to commit a disproportionately large percentage of their portfolio to a single iron condor. When the market moves violently against an over-leveraged position, the consequences can be devastating.

Consider a trader with a $50,000 portfolio. They might see an iron condor on SPY with a 0.15 delta short call and put, offering a potential credit of $1.00 ($100 per contract) for a $5 wide spread. The maximum loss on this trade is $4.00 ($400 per contract), excluding commissions.

If this trader decides to sell 10 contracts, their potential credit is $1,000, and their maximum loss is $4,000. This $4,000 max loss represents 8% of their total portfolio. While 8% might seem acceptable to some, it's a single trade's maximum potential loss.

What if they have three such trades on simultaneously? That's 24% of their portfolio at risk from maximum loss events across three uncorrelated (or perhaps even correlated) positions.

Our backtesting data for SPX iron condors, utilizing our proprietary 30-45 DTE, 0.15 delta short strike, IV Rank > 30 entry criteria, and 50% profit target/200% loss stop exit rules, shows a win rate of approximately 80-85% over various market cycles. While this is a robust edge, it also implies a 15-20% chance of hitting a stop loss, or worse, a maximum loss if the stop is missed or gapped through.

If each losing trade represents 8% of the portfolio, a string of just three consecutive losses (a statistical possibility, albeit low) would erode 24% of the capital. This is a significant drawdown that can be psychologically debilitating and make recovery extremely challenging.

Key Takeaway: The "max loss" on a single iron condor should not be the sole determinant of position size. Instead, it should be viewed in the context of the entire portfolio's risk tolerance and the potential for multiple concurrent losing trades.

Defining Your Portfolio's Risk Tolerance: The "Core Capital at Risk" Metric

At Volatility Anomaly, we advocate for a top-down approach to position sizing, starting with your overall portfolio's risk tolerance. This isn't just about the maximum loss on a single trade; it's about the aggregate capital you are willing to expose to market risk at any given time.

We introduce the concept of "Core Capital at Risk" (CCAR).

Core Capital at Risk (CCAR): The absolute maximum percentage of your total trading capital you are willing to lose in a worst-case scenario over a defined period (e.g., a month or a quarter), or from a complete systemic failure of your current open positions.

For most experienced options traders, we recommend a CCAR of 5-10% of their total trading capital. For more aggressive traders with a higher risk appetite and robust psychological resilience, this might stretch to 15%, but rarely higher.

This CCAR then dictates the maximum aggregate "defined risk" you can have on across all open positions.

Let's revisit our $50,000 portfolio example with a CCAR of 10%. This means the trader is willing to risk a maximum of $5,000 (10% of $50,000) across all open iron condor positions at any given time.

Calculating Maximum Allowable Contracts per Trade

Once your CCAR is established, you can then determine the maximum number of contracts for any single iron condor. This calculation must consider the defined risk of the spread.

Formula:

Maximum Contracts = (Portfolio CCAR * Total Portfolio Value) / (Max Loss per Contract * Number of Simultaneous Trades)

Let's refine this. A more practical approach is to determine the maximum capital allocated to each trade, given your CCAR and the number of simultaneous trades you anticipate.

Example:

- Total Portfolio Value: $50,000

- CCAR: 10% ($5,000)

- Anticipated Simultaneous Trades: 5 (e.g., SPX, QQQ, IWM, XLE, XLF)

- Max Loss per Contract (SPY Iron Condor): $400

If you have 5 simultaneous trades, and your total CCAR is $5,000, that means each trade, on average, should not exceed a maximum loss exposure of $1,000 ($5,000 / 5 trades).

Therefore, for the SPY iron condor with a $400 max loss per contract:

Maximum Contracts per SPY Trade = $1,000 (Allocated Max Loss) / $400 (Max Loss per Contract) = 2.5 contracts.

Since you can't trade half a contract, you would round down to 2 contracts.

This means, with a $50,000 portfolio and a 10% CCAR spread across 5 simultaneous trades, you would trade 2 contracts of the $5-wide SPY iron condor.

- Potential Credit (2 contracts): $200

- Maximum Loss (2 contracts): $800 (1.6% of portfolio)

This approach ensures that even if all 5 simultaneous trades hit their maximum loss, your total portfolio drawdown would be $4,000 ($800 x 5), which is 8% of your portfolio — well within your 10% CCAR. This provides a robust buffer against worst-case scenarios.

The Role of Our 200% Loss Stop

It's crucial to integrate our systematic 200% loss stop into this calculation. While the defined maximum loss is the theoretical worst-case, our system aims to exit losing trades much earlier. For an iron condor where you collect $1.00 in credit, a 200% loss stop means exiting when the trade is down $2.00 from the credit received (i.e., the mark-to-market value of the spread is -$1.00, or the premium has decayed to $0.00 and then moved against you by $2.00).

This means your expected loss per contract is $200, not $400.

If we apply the 200% loss stop to our calculation:

Maximum Contracts per SPY Trade = $1,000 (Allocated Max Loss) / $200 (Expected Loss per Contract with Stop) = 5 contracts.

This allows for a larger position size while still adhering to the spirit of the CCAR, assuming your stop-loss execution is consistent. However, it's vital to acknowledge that stop losses can be gapped through, especially in volatile markets or during overnight sessions.

Therefore, while the 200% stop is your primary defense, the defined max loss should always be the ultimate arbiter of your position sizing for capital allocation purposes. It's the "what if everything goes wrong" number.

Volatility Anomaly Recommendation: Always size your positions based on the defined maximum loss per contract when determining your CCAR allocation. The 200% loss stop is a risk mitigation tool, not a license to over-leverage.

Dynamic Position Sizing: Adapting to Volatility and IV Rank

Static position sizing, while simple, fails to account for changing market conditions. Volatility, specifically implied volatility (IV), plays a critical role in iron condor pricing and risk. Higher IV generally means wider bid-ask spreads, potentially larger credits, but also a higher probability of significant price swings that could challenge your short strikes.

Our system emphasizes entering trades when IV Rank > 30. This ensures we are selling premium when it is relatively rich. However, the level of IV Rank can also inform position sizing.

The Kelly Criterion (Simplified for Options)

The Kelly Criterion is a mathematical formula used to determine the optimal size of a series of bets to maximize the long-term growth rate of wealth. While directly applying the full Kelly Criterion to complex options strategies like iron condors is challenging due to varying probabilities and payouts, its underlying principle — sizing bets proportionally to your edge and inversely to risk — is highly relevant.

A simplified interpretation for iron condors suggests that when your edge is stronger (e.g., higher IV Rank, better historical win rates for a specific underlying), you can slightly increase your allocation. Conversely, when your edge is weaker (lower IV Rank, uncertain market conditions), you should reduce it.

Volatility Anomaly's Dynamic Sizing Framework:

- Baseline Allocation (CCAR-derived): This is your foundational position size based on the defined max loss and your CCAR, as discussed above.

- Volatility-Adjusted Scaling:

- IV Rank 30-50: Use your baseline allocation. This is our standard entry zone.

- IV Rank 50-70: Consider a slight increase of 10-20% in contracts, only if the underlying's historical behavior in this IV range still supports your win rate assumptions and your CCAR allows for it. For example, if your baseline is 2 contracts, you might increase to 3.

- IV Rank > 70: While premium is exceptionally rich, this often signifies extreme market stress (e.g., crash, major event). While tempting, these environments are prone to rapid, unpredictable moves. We generally advocate for reducing position size by 10-20% from baseline, or even waiting for IV to subside. The potential for gapping through stops is significantly higher. The allure of high credit can mask the increased risk of extreme outliers.

- IV Rank < 30: Our system generally avoids entries here. If you are already in a trade and IV Rank drops, it suggests a calmer market, which can be beneficial for time decay, but new entries are less attractive.

Practical Application with SPX:

SPX iron condors often have a higher max loss per contract due to the larger notional value. A typical $10-wide SPX iron condor might have a max loss of $900 per contract.

- Portfolio: $100,000

- CCAR: 8% ($8,000)

- Anticipated Simultaneous Trades: 4 (SPX, QQQ, IWM, XLK)

- Allocated Max Loss per Trade: $2,000 ($8,000 / 4)

For an SPX iron condor with a $900 max loss per contract:

Maximum Contracts = $2,000 / $900 = 2.22 contracts. Round down to 2 contracts.

Now, apply volatility scaling:

- If SPX IV Rank is 40: Trade 2 contracts.

- If SPX IV Rank is 60: You might consider 3 contracts, but only if your total CCAR still allows for it ($2,700 max loss for 3 contracts, leaving $5,300 for the other 3 trades). This requires careful monitoring of your aggregate risk.

- If SPX IV Rank is 80: Revert to 1-2 contracts, or even consider waiting. Extreme IV often precedes extreme moves.

Sector Rotation and Diversification:

Our emphasis on sector rotation (e.g., XLE, XLF, XLK, XLI) is not just about finding the best IV Rank opportunities, but also about diversifying risk. Placing multiple iron condors on highly correlated instruments (e.g., SPY and QQQ during a tech-led rally/sell-off) effectively concentrates risk, even if they are technically separate trades.

Volatility Anomaly's Diversification Principle: When calculating "Anticipated Simultaneous Trades," consider the correlation between the underlying assets. If you have 3 trades on highly correlated tech ETFs (XLK, SMH, FDN), treat them more like 1-2 concentrated positions for risk allocation purposes. Aim for diversification across different sectors (Energy, Financials, Healthcare, Tech, Industrials) to truly spread your risk.

The Absolute Stop Loss: Protecting Your Portfolio from Catastrophe

While our 200% loss stop is designed to manage individual trade risk, every iron condor trader needs an absolute portfolio-level stop loss. This is the point at which you cease trading, reassess your strategy, and protect your remaining capital.

Why an Absolute Stop Loss is Non-Negotiable

No strategy, regardless of its statistical edge, is immune to black swan events or prolonged adverse market conditions. A series of unexpected market shocks can rapidly erode capital. Without an absolute stop, emotional decision-making can take over, leading to "revenge trading" or doubling down on losing positions, accelerating capital depletion.

Volatility Anomaly's Absolute Stop Loss Recommendation:

We recommend setting an absolute portfolio drawdown limit of 15-20% from your peak equity.

Example:

- Starting Portfolio: $100,000

- Absolute Stop Loss: 15% drawdown ($15,000)

- If your portfolio drops to $85,000, you stop trading.

This doesn't mean you abandon iron condors forever. It means you:

- Cease all new entries.

- Manage existing positions defensively: Consider closing them early for smaller losses, or adjusting them if appropriate, but avoid adding new risk.

- Review and Analyze: What went wrong? Was it strategy execution? Market conditions? Position sizing?

- Re-evaluate: Only resume trading once you have a clear understanding of the drawdown's causes and a refined plan.

This absolute stop loss acts as a circuit breaker, preventing a death spiral and preserving capital for future opportunities. It's the ultimate form of risk management.

The "Max Loss" vs. "Expected Loss" Conundrum Revisited

It's critical to understand the distinction between the theoretical maximum loss of an iron condor and the expected loss when employing systematic exit rules.

- Maximum Loss (Defined Risk): This is the difference between the strike prices minus the credit received. For a $5 wide spread collecting $1.00, the max loss is $4.00 ($400 per contract). This is the number you must use for initial position sizing based on your CCAR.

- Expected Loss (with 200% Stop): Our system dictates closing a losing trade when the loss reaches 200% of the credit received. For a $1.00 credit, this means exiting when the trade is down $2.00. This translates to an actual loss of $200 per contract.

While our 200% stop significantly reduces the average loss per losing trade, it is not foolproof. Gaps, flash crashes, or extremely rapid moves can cause the market price to blow past your stop level, leading to a loss closer to, or even exceeding, the defined max loss.

Volatility Anomaly's Prudent Approach:

Always size your positions assuming the defined maximum loss for your CCAR calculations. This is the most conservative and responsible approach. The 200% stop is a powerful tool to mitigate these potential maximum losses, but it should not be relied upon as the sole risk determinant for initial capital allocation.

This conservative sizing allows your portfolio to absorb the occasional "gapped through stop" event without catastrophic consequences.

Practical Implementation Checklist for Iron Condor Traders

To summarize and provide actionable steps, here’s a checklist for implementing robust position sizing and risk management:

- Determine Your Total Trading Capital: Be honest about the capital you are willing to risk in the market.

- Establish Your Core Capital at Risk (CCAR):

- Conservative: 5% of total capital

- Moderate: 8-10% of total capital

- Aggressive: 12-15% of total capital (exercise extreme caution)

- Estimate Your Number of Simultaneous Trades: Consider diversification. Aim for 3-5 uncorrelated positions.

- Calculate Maximum Allowable Defined Risk per Trade:

- `Max Risk per Trade = (CCAR * Total Capital) / Number of Simultaneous Trades`

- Calculate Maximum Contracts per Trade (Based on Max Loss):

- `Max Contracts = Max Risk per Trade / Max Loss per Contract`

- Always round down to the nearest whole contract.

- Implement Dynamic Sizing (Optional, but Recommended):

- Adjust contract size slightly based on IV Rank (e.g., -10%

#VolatilityAnomaly · #IVRank · #OptionsTrading · #VRP

You Might Also Like

Volatility Anomaly

Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance

Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance In the world of options trading, strategies like the Iron Condor are highly popular for their ability to generate consistent

Jan 1970

Volatility Anomaly

Gamma Risk in Iron Condors: Understanding the Danger Zone Near Expiration

Gamma Risk in Iron Condors: Understanding the Danger Zone Near Expiration As options traders, we often seek strategies that offer defined risk and a high probability of profit. The iron condor, a staple in many portfolios, perfectly embodies this philosophy. By selling out-of-the

Jan 1970

YOU MIGHT ALSO LIKE

Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance

Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance Portfolio-Level Hedging for Iron…

Read articleGamma Risk in Iron Condors: Understanding the Danger Zone Near Expiration

Gamma Risk in Iron Condors: Understanding the Danger Zone Near Expiration As options traders, we often seek st…

Read articleThe 50% Profit Target Rule: Why Closing Early Improves Your Long-Term Returns

The 50% Profit Target Rule: Why Closing Early Improves Your Long-Term Returns In the dynamic world of options…

Read articleThis article is for educational purposes only and does not constitute financial or investment advice. Options trading involves significant risk of loss and is not suitable for all investors. Past performance is not indicative of future results.