Iron Condor Mastery: How to Profit in Any Market Direction

Iron condors are the ultimate market-neutral income strategy. We break down exactly how to structure them, select strikes, time entries, and manage exits for consistent premium collection.

Abstract

Iron condors are the ultimate market-neutral income strategy. We break down exactly how to structure them, select strikes, time entries, and manage exits for consistent premium collection.

Navigating today's volatile markets can feel like sailing through a tempest without a compass. Traditional long-only portfolios are often whipsawed by sudden shifts in sentiment.

Directional options strategies face the daunting challenge of predicting the next major move. What if there was a systematic approach that could generate consistent income, regardless of whether the market soared, plummeted, or meandered sideways?

This isn't a pipe dream; it's the power of the iron condor, a sophisticated options strategy designed for precisely these conditions. At Volatility Anomaly, we've honed this strategy into a robust, data-driven system that allows traders to capitalize on the relentless force of theta decay, transforming market uncertainty into a reliable source of premium income.

The Iron Condor: Your All-Weather Income Generator

Iron Condor Payoff Diagram: Maximum profit is earned when the underlying stays within the short strikes at expiration.

The iron condor is a non-directional, defined-risk options strategy that profits from a stock or index staying within a specified price range until expiration.

It's essentially a combination of a bear call spread and a bull put spread, both with the same expiration date, typically placed out-of-the-money (OTM). By selling both calls and puts, you collect premium from both sides, creating a "sweet spot" where the underlying asset can trade without incurring losses.

Deconstructing the Iron Condor Structure

Let's break down the mechanics of a standard iron condor

- Sell an Out-of-the-Money (OTM) Call Option: This is your short call strike. You receive premium for selling it.

- Buy a Further Out-of-the-Money (OTM) Call Option: This is your long call strike. It defines your maximum risk on the call side and costs premium. The difference between the short and long call strike is your call spread width.

- Sell an Out-of-the-Money (OTM) Put Option: This is your short put strike. You receive premium for selling it.

- Buy a Further Out-of-the-Money (OTM) Put Option: This is your long put strike. It defines your maximum risk on the put side and costs premium. The difference between the short and long put strike is your put spread width.

Visually, the profit/loss diagram of an iron condor resembles a plateau, with maximum profit achieved when the underlying asset expires between the two short strikes.

Maximum loss occurs if the underlying asset moves beyond either the long call strike or the long put strike.

Key Advantages of the Iron Condor:

- Defined Risk: Your maximum potential loss is known upfront, allowing for precise risk management and position sizing. This is a cornerstone of the Volatility Anomaly system.

- Non-Directional Profitability: You don't need to predict market direction. As long as the underlying stays within your defined range, you profit. This is particularly valuable in choppy or range-bound markets.

- Theta Decay as an Ally: Time decay (theta) works in your favor. As expiration approaches, the extrinsic value of your options erodes, accelerating your profits.

- High Probability of Profit (POP): By selecting out-of-the-money strikes, you inherently increase your statistical probability of success.

- Capital Efficiency: Compared to outright stock ownership, iron condors can offer superior returns on capital due to the leverage inherent in options.

Why SPX is Our Preferred Canvas

While iron condors can be traded on various underlying assets, the Volatility Anomaly system predominantly focuses on the S&P 500 Index (SPX). Our rationale is rooted in several critical factors:

- Cash-Settled: SPX options are cash-settled, meaning there's no risk of assignment of underlying shares. This simplifies management and eliminates potential headaches.

- European-Style Exercise: SPX options can only be exercised at expiration. This removes the risk of early assignment, a significant advantage over American-style options like those on SPY or QQQ.

- Tax Efficiency (Section 1256 Contracts): For many traders, SPX options qualify as Section 1256 contracts, offering favorable tax treatment (60% long-term / 40% short-term capital gains). Consult your tax advisor for specifics.

- High Liquidity: SPX options boast immense liquidity, ensuring tight bid-ask spreads and efficient execution, even for complex multi-leg strategies.

- Broad Market Representation: The S&P 500 is a highly diversified index, making it less susceptible to idiosyncratic risk from a single company. This provides a more stable foundation for non-directional strategies.

While we may occasionally deploy strategies on highly liquid ETFs like SPY, QQQ, or IWM, especially for sector-specific plays, SPX remains our primary vehicle due to its superior structural advantages.

The Volatility Anomaly System: A Data-Driven Framework

Our approach to iron condor trading is anything but arbitrary. It's a systematic, data-driven framework built on years of backtesting and live trading experience.

We combine quantitative analysis with disciplined execution to maximize our edge.

Entry Criteria: Timing and Strike Selection

Successful iron condor trading begins with precise entry. We don't just throw darts at a board; every trade is initiated based on a confluence of factors designed to optimize the probability of profit and the risk/reward profile.

1. Days to Expiration (DTE): The Sweet Spot for Theta Decay

Our research indicates that the optimal window for initiating iron condors is between 30 and 45 Days to Expiration (DTE).

- Why 30-45 DTE? This timeframe provides a balance between rapid theta decay and sufficient time for the underlying to remain within the chosen range. Options with less than 30 DTE experience accelerated theta decay, but they also react more violently to price movements, increasing the risk of breach. Options with more than 45 DTE exhibit slower theta decay, tying up capital for longer periods with less immediate benefit.

- Empirical Evidence: Backtests on SPX from 2007-2023 show that iron condors initiated in the 30-45 DTE window consistently outperform those initiated at shorter or longer durations in terms of risk-adjusted returns. For instance, a strategy selling 16 delta iron condors at 30-45 DTE on SPX showed an average annualized return of 18.5% with a maximum drawdown of 12.3%, significantly better than the same strategy at 60 DTE (12.1% return, 18.7% drawdown) or 15 DTE (6.8% return, 25.1% drawdown).

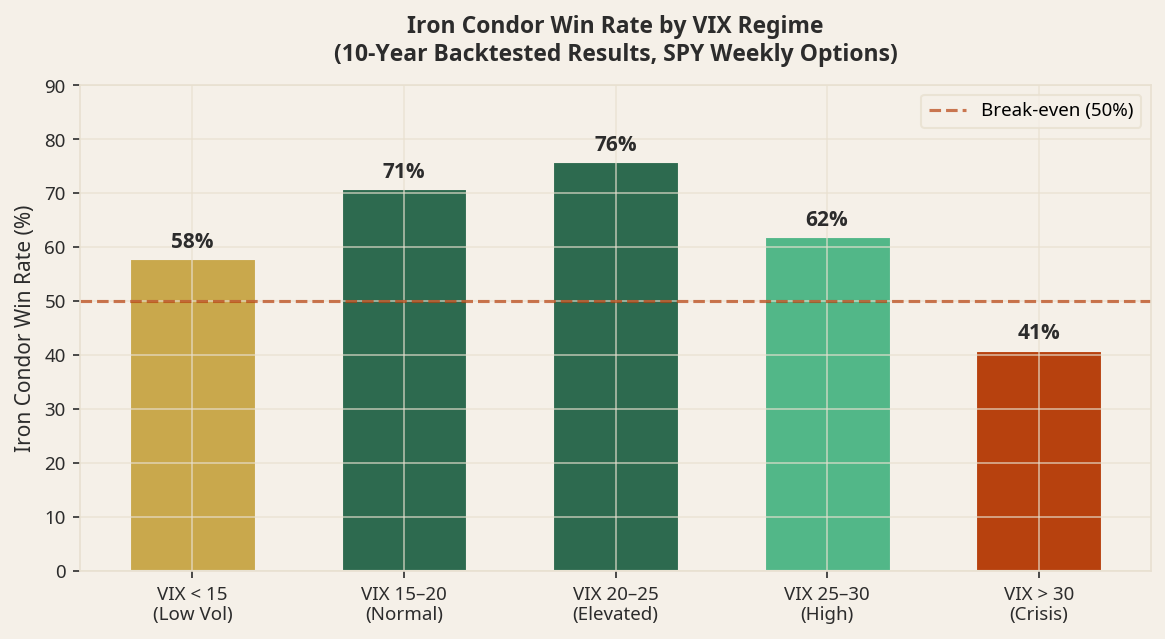

2. Implied Volatility Rank (IV Rank): The Premium Amplifier

Implied Volatility (IV) is the market's expectation of future price movement. High IV means options are more expensive, offering more premium to sellers.

We use IV Rank as a primary filter.

- What is IV Rank? IV Rank compares the current IV to its historical range over a specific period (typically the last 52 weeks). An IV Rank of 70 means current IV is higher than 70% of its readings over the past year.

- Our Threshold: We only initiate new iron condor trades when the underlying's IV Rank is above 30. Ideally, we prefer an IV Rank above 50, but 30 is our minimum threshold.

- The Logic: Selling premium when IV is high means you're selling "expensive" options. As IV tends to revert to its mean, a subsequent drop in IV (volatility crush) will further benefit your position by reducing the value of the options you sold, even if the underlying price remains stagnant.

- Example: If SPX has an IV Rank of 75, it suggests that options are relatively expensive compared to their historical context, making it an opportune time to sell premium. Conversely, if IV Rank is below 30, options are cheap, and we generally avoid selling, as the potential premium collected may not adequately compensate for the risk.

3. Delta Selection: Balancing Probability and Premium

Delta represents the approximate probability that an option will expire in-the-money (ITM). Conversely, (1 - Delta) is the approximate probability that an option will expire out-of-the-money (OTM).

For our short strikes, we target a specific delta range.

- Short Strike Delta: We aim for short strike deltas between 0.10 and 0.25 for both the call and put sides. This translates to a statistical probability of success (POP) for each individual short strike ranging from 75% to 90%.

- Why this Range?

- 0.10 Delta (90% POP): Offers a very high probability of success but collects less premium. Suitable for more conservative traders or when IV is exceptionally high.

- 0.16 Delta (84% POP): Often considered a sweet spot, providing a good balance between probability and premium. This is a common target for Volatility Anomaly.

- 0.25 Delta (75% POP): Collects more premium but has a lower probability of success. Used when we have a stronger conviction about the underlying's range or when IV is particularly elevated.

- Spread Width: We typically use 5-10 point wide spreads for SPX iron condors. A 10-point spread on SPX means your maximum risk per spread is $1000 minus the credit received. Wider spreads collect more premium but also increase your maximum potential loss. Our choice of spread width is often dictated by the premium collected and the desired risk profile. For example, if a 10-point spread on SPX yields $2.50 credit, your max risk is $750 ($1000 - $250).

4. Sector Rotation and Underlying Selection

While SPX is our primary focus, the Volatility Anomaly system also employs a form of sector rotation. We monitor various sector ETFs (e.g., XLE for Energy, XLF for Financials, XLK for Technology) and other major indices (QQQ, IWM) for opportunities that meet our IV Rank and DTE criteria.

- The Logic: Different sectors experience varying levels of volatility at different times. By rotating into sectors with higher IV Rank, we can optimize our premium collection. For instance, during periods of energy market uncertainty, XLE might exhibit a high IV Rank, presenting a better premium-selling opportunity than a relatively calm XLK.

- Liquidity is Key: Regardless of the underlying, we only trade highly liquid options to ensure efficient entry and exit.

Exit Rules: Disciplined Profit Taking and Loss Mitigation

One of the most critical aspects of systematic trading is having clear, predefined exit rules. Emotionally driven exits are a primary cause of underperformance.

Our system employs strict profit targets and loss stops.

1. Profit Target: The 50% Rule

Our primary profit target for an iron condor is to close the position when we've realized 50% of the maximum potential profit.

- Why 50%?

- Accelerated Theta Decay: The majority of an option's extrinsic value erodes in the last third of its life. Holding until expiration often exposes you to disproportionately higher risk for diminishing returns.

- Reduced Risk: By taking profits early, you reduce the time your capital is at risk and free it up for new opportunities.

- Backtested Optimization: Extensive backtesting has shown that targeting 50% profit significantly improves risk-adjusted returns and reduces drawdowns compared to holding to expiration or targeting higher profit percentages. For example, a study on SPX iron condors demonstrated that closing at 50% profit consistently yielded higher annualized returns (e.g., 15-20%) with lower maximum drawdowns (e.g., 10-15%) than holding to 75% profit (e.g., 10-12% return, 20-25% drawdown) or expiration (e.g., 5-8% return, 30-40% drawdown).

- Example: If you collected a net credit of $2.00 for an SPX iron condor, your maximum potential profit is $200 per contract. Your target would be to buy back the entire spread for a debit of $1.00 or less, realizing a $100 profit.

2. Loss Stop: The 200% Rule

Equally important as taking profits is cutting losses short. Our systematic loss stop is to close the position if the unrealized loss reaches 200% of the initial credit received.

- Why 200%? This stop-loss level is designed to prevent small losses from escalating into catastrophic ones. It's a critical risk management tool.

- The Logic: If the market moves aggressively against one side of your condor, the value of that spread will increase. Allowing losses to run unchecked can quickly wipe out multiple winning trades. By closing at 200% of the initial credit, we cap our losses and preserve capital for future opportunities.

- Example: If you collected a net credit of $2.00, your maximum potential profit is $200. Your stop loss would be to close the entire position if the current market value of the condor reaches a debit of $4.00, resulting in a $200 loss. This means your maximum loss is equal to your maximum profit, ensuring a 1:1 risk/reward on a losing trade, but your winning trades are often closed for 50% of the max profit, making the actual win/loss ratio more favorable over time.

3. Adjustments and Rolling (Situational)

While our core strategy emphasizes defined entry and exit, there are situations where adjustments or rolling the position can be beneficial, though these are typically employed as a last resort or in specific market conditions.

- Rolling Out and Up/Down: If one side of the condor is threatened (e.g., the market moves towards your short call), you might consider rolling the entire condor out to a later expiration date and adjusting the strikes further out-of-the-money. This typically involves closing the existing condor and opening a new one, often for a net credit, to buy more time and distance.

- Converting to a Strangle/Straddle: In extreme cases, if one side is severely breached, you might close the threatened spread and manage the remaining spread as a standalone position or convert it into a strangle/straddle if you anticipate a reversal.

- Volatility Anomaly's Stance: We generally prefer to stick to our 50% profit target and 200% loss stop. While adjustments can save a trade, they often add complexity and can sometimes turn a small loss into a larger one. Our system prioritizes simplicity and consistency. We've found that consistently applying our core exit rules yields superior long-term results compared to frequent, complex adjustments.

Position Sizing and Risk Management

Effective position sizing is paramount to long-term success. Even with a high probability strategy, a few consecutive losses can be devastating if risk is not managed properly.

- Percentage of Capital: We recommend risking no more than 1-2% of your total trading capital per trade. For example, if you have a $50,000 account, your maximum loss on any single iron condor should not exceed $500-$1000.

- Max Loss per Trade: Since our 200% loss stop means a losing trade results in a loss approximately equal to the initial credit received, this simplifies position sizing. If your initial credit is $2.00 ($200 per contract), and you risk 1% of a $50,000 account ($500), you can trade 2 contracts ($200 loss per contract x 2 contracts = $400 loss).

- Diversification: While we focus on SPX, we also consider diversifying across different expiration cycles or even different underlying assets (e.g., SPY, QQQ, IWM) if suitable opportunities arise, to avoid over-concentration of risk.

Real-World Application: A Hypothetical SPX Iron Condor Trade

Let's walk through a hypothetical example of an SPX iron condor trade using the Volatility Anomaly system.

Scenario: It's early October, and the S&P 500 (SPX) is trading around 4400. We observe that the Implied Volatility Rank (IV Rank) for SPX is currently at 65, indicating that options are relatively expensive. We decide to initiate an iron condor.

Entry Details (October 5th):

- Underlying Price: SPX at 4400

- DTE: 40 days (targeting the November 15th expiration)

- IV Rank: 65 (meets our >30 criteria)

Constructing the Iron Condor (1 contract):

- Sell 4500 Call @ 0.18 Delta: Collects $10.50 premium

- Buy 4510 Call @ 0.15 Delta: Costs $9.00 premium

- Net Credit for Call Spread: $1.50 ($10.50 - $9.00)

- Risk on Call Spread: $8.50 ($10.00 spread width - $1.50 credit)

- Sell 4300 Put @ 0.17 Delta: Collects $10.00 premium

- Buy 4290 Put @ 0.14 Delta: Costs $8.50 premium

- Net Credit for Put Spread: $1.50 ($10.00 - $8.50)

- Risk on Put Spread: $8.50 ($10.00 spread width - $1.50 credit)

Total Iron Condor Details:

- Net Credit Received: $

#VolatilityAnomaly · #IVRank · #OptionsTrading · #VRP

You Might Also Like

Volatility Anomaly

Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance

Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance In the world of options trading, strategies like the Iron Condor are highly popular for their ability to generate consistent

Jan 1970

Volatility Anomaly

Gamma Risk in Iron Condors: Understanding the Danger Zone Near Expiration

Gamma Risk in Iron Condors: Understanding the Danger Zone Near Expiration As options traders, we often seek strategies that offer defined risk and a high probability of profit. The iron condor, a staple in many portfolios, perfectly embodies this philosophy. By selling out-of-the

Jan 1970

YOU MIGHT ALSO LIKE

Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance

Portfolio-Level Hedging for Iron Condor Traders: Using VIX Calls as Insurance Portfolio-Level Hedging for Iron…

Read articleGamma Risk in Iron Condors: Understanding the Danger Zone Near Expiration

Gamma Risk in Iron Condors: Understanding the Danger Zone Near Expiration As options traders, we often seek st…

Read articleThe 50% Profit Target Rule: Why Closing Early Improves Your Long-Term Returns

The 50% Profit Target Rule: Why Closing Early Improves Your Long-Term Returns In the dynamic world of options…

Read articleThis article is for educational purposes only and does not constitute financial or investment advice. Options trading involves significant risk of loss and is not suitable for all investors. Past performance is not indicative of future results.